Shari’ah Supervision

Guidance Note Re Annual Shari'ah Report of Internal Shari'ah Supervision Committee*

N 5330/2020 Effective from 10/12/2020The Central Bank is pleased to attach herewith the Guidance Note Re Annual Shari’ah Report of Internal Shari’ah Supervision Committee, which applies to licensed financial institutions that conduct all or part of their activities and businesses in accordance with the provisions of Islamic Shari’ah (Islamic Financial Institutions).

This Guidance Note must be read in conjunction with the regulations, standards and resolutions issued by the Central Bank and the Higher Shari’ah Authority.

This Guidance Note is mandatory and effective from the date of this notice.

Please bring this Guidance Note to the attention of the board of directors of your institution at the next board meeting.

*This document was drafted in Arabic and translated to English. In case of any differences in interpretation, the Arabic version shall prevail.

Article (1) Introduction

1.1. This Guidance Note Re Annual Shari’ah Report of Internal Shari’ah Supervision Committee (“Guidance Note” or “Note”) complements the requirements outlined in:

- Decretal Federal Law No. (14) of 2018 Regarding the Central Bank and Organization of Financial Institutions and Activities; and

- Standard Re Shari’ah Governance for Islamic Financial Institutions issued by the Central Bank.

with the aim to promote development of the banking system and to ensure its effectiveness and efficiency.

- 1.2. Islamic Financial Institutions (“IFIs”) are required to have Shari’ah governance policies and mechanisms to ascertain that Annual Shari’ah Report that is issued by the Internal Shari’ah Supervision Committee (“Annual Shari’ah Report”) is compliant with requirements outlined in this Guidance Note, and applicable standards and regulations.

- 1.3. Where the Guidance Note contains a stipulation (in an article) to provide information, or undertake certain measures, or address particular terms, as a minimum requirement, the Central Bank may impose (new) requirements additional to those specified in the relevant article (of the Guidance Note).

Article (2) Objectives

- 2.1. The Guidance Note contains guidance aimed at facilitating implementation of the requirements related to the issuance of Annual Shari’ah Report.

- 2.2. The Guidance Note provides clarity on the supervisory expectations with respect to Annual Shari’ah Report.

- 2.1. The Guidance Note contains guidance aimed at facilitating implementation of the requirements related to the issuance of Annual Shari’ah Report.

Article (3) Scope of Application

- 3.1. The Guidance Note applies to all IFIs.

- 3.2. The Guidance Note must be read in conjunction with the standards and resolutions issued by Higher Shari’ah Authority (HSA) and notified to IFIs.

- 3.1. The Guidance Note applies to all IFIs.

Article (4) General Requirements for Issuing the Annual Shari'ah Report

- 4.1. The Annual Shari’ah Report represents annual disclosure of the Internal Shari’ah Supervision Committee (ISSC) on the level of IFI’s compliance with Islamic Shari’ah. Accordingly, responsibility for preparing the annual Shari’ah report rests with the ISSC of IFI within the mechanisms and requirements stipulated in the Guidance Note.

- 4.2. The Annual Shari’ah Report should be presented at the general assembly in accordance with the applicable regulatory requirements.

- 4.3. The Annual Shari’ah Report shall be submitted to HSA for review and approval prior to its submission at the general assembly.

- 4.4. The Annual Shari’ah Report must be submitted to the HSA, no later than two (2) months from end of the financial year.

- 4.5. The ISSC must verify accuracy and validity of all information in the Annual Shari’ah Report before its submission to the HSA.

- 4.6. The Board must ensure that the Annual Shari’ah Report is submitted to HSA for review and approval prior for its submission at the general assembly.

- 4.7. The ISSC must ascertain that all information required to be stated in the Annual Shari’ah Report (as stipulated in the template in article No. 5.3) are included in the designated places of the report before submitting it to HSA.

- 4.8. The ISSC must ensure that all duties fulfilled by the ISSC, as outlined in the Annual Shari’ah Report, are well documented for audit purposes.

- 4.9. IFI shall publish the Annual Shari’ah Report in the IFI’s disclosures of the financial statement and other available means.

- 4.1. The Annual Shari’ah Report represents annual disclosure of the Internal Shari’ah Supervision Committee (ISSC) on the level of IFI’s compliance with Islamic Shari’ah. Accordingly, responsibility for preparing the annual Shari’ah report rests with the ISSC of IFI within the mechanisms and requirements stipulated in the Guidance Note.

Article (5) Template for the Annual Shari'ah Report

- 5.1. Template of the Annual Shari’ah Report (as per below) represents the principal information and disclosures, and minimum requirements for information that should be included in the report.

- 5.2. The ISSC may add other information to the Annual Shari’ah Report, if necessary, according to the template in the Guidance Note.

- 5.1. Template of the Annual Shari’ah Report (as per below) represents the principal information and disclosures, and minimum requirements for information that should be included in the report.

(5/3) Template for the Annual Shari'ah Report (English)

Annual Report of the Internal Shari'ah Supervision Committee of (name of the financial institution)

Issued on: (issue date)

To: Shareholders of (name of the Financial Institution) (“the Institution”)

After greetings,

Pursuant to requirements stipulated in the relevant laws, regulations and standards (“the Regulatory Requirements”), the Internal Shari’ah Supervision Committee of the Institution (“ISSC”) presents to you the ISSC’s Annual Report (in case of Islamic windows add: (regarding Shari’ah compliant businesses and operations of the Institution)) for the financial year ending on 31 December --------- (“Financial Year”).

- Responsibility of the ISSC

In accordance with the Regulatory Requirements and the ISSC’s charter, the ISSC’s responsibility is stipulated as to:- undertake Shari’ah supervision of all businesses, activities, products, services, contracts, documents and business charters of the Institution; and the Institution’s policies, accounting standards, operations and activities in general, memorandum of association, charter, financial statements, allocation of expenditures and costs, and distribution of profits between holders of investment accounts and shareholders (“Institution’s Activities”) and issue Shari’ah resolutions in this regard, and

- determine Shari’ah parameters necessary for the Institution’s Activities, and the Institution’s compliance with Islamic Shari’ah within the framework of the rules, principles, and standards set by the Higher Shari’ah Authority (“HSA”) to ascertain compliance of the Institution with Islamic Shari’ah.

The senior management is responsible for compliance of the Institution with Islamic Shari’ah in accordance with the HSA’s resolutions, fatwas, and opinions, and the ISSC’s resolutions within the framework of the rules, principles, and standards set by the HSA (“Compliance with Islamic Shari’ah”) in all Institution’s Activities, and the Board bears the ultimate responsibility in this regard.

- undertake Shari’ah supervision of all businesses, activities, products, services, contracts, documents and business charters of the Institution; and the Institution’s policies, accounting standards, operations and activities in general, memorandum of association, charter, financial statements, allocation of expenditures and costs, and distribution of profits between holders of investment accounts and shareholders (“Institution’s Activities”) and issue Shari’ah resolutions in this regard, and

- Shari’ah Standards

In accordance with the HSA’s resolution (No. 18/3/2018), and with effect from 01/09/2018, the ISSC has abided by the Shari’ah standards issued by the Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) as minimum Shari’ah requirements, in all fatwas, approvals, endorsements and recommendations, relating to the Institution’s Activities without exception. - Duties Fulfilled by the ISSC During the Financial Year

The ISSC conducted Shari’ah supervision of the Institution’s Activities by reviewing those Activities, and monitoring them through the internal Shari’ah control division or section, internal Shari’ah audit, and (if applicable) external Shari’ah audit, in accordance with the ISSC’s authorities and responsibilities, and pursuant to the Regulatory Requirements in this regard. The ISSC’s activities included the following:- Convening (number) meetings during the year.

- Issuing fatwas, resolutions and opinions on matters presented to the ISSC in relation to the Institution’s Activities.

- Monitoring compliance of policies, procedures, accounting standards, product structures, contracts, documentation, business charters, and other documentation submitted by the Institution to the ISSC for approval.

- Ascertaining the level of compliance of allocation of expenditures and costs, and distribution of profits between investment accounts holders and shareholders with parameters set by the ISSC.

- Supervision through the internal Shari’ah control division or section, internal Shari’ah audit, and (if applicable) external Shari’ah audit, of the Institution’s Activities including supervision of executed transactions and adopted procedures on the basis of samples selected from executed transactions, and reviewing reports submitted in this regard.

- Providing guidance to relevant parties in the Institution — to rectify (where possible) incidents cited in the reports prepared by internal Shari’ah control division or section, internal Shari’ah audit, and/or (if applicable) external Shari’ah audit — and issuing of resolutions to set aside revenue derived from transactions in which non-compliances were identified for such revenue to be disposed towards charitable purposes.

- Approving corrective and preventive measures related to identified incidents to preclude their reoccurrence in the future.

- Specifying the amount of Zakat due on each share of the Institution (if applicable).

- Communicating with the Board and its subcommittees, and the senior management of the Institution (as needed) concerning the Institution’s compliance with Islamic Shari’ah.

- (add other works that the ISSC wants to mention in this report)

The ISSC sought to obtain all information and interpretations deemed necessary in order to reach a reasonable degree of certainty that the Institution is compliant with Islamic Shari’ah. (the phrase “External Shari’ah audit” is included in the report if applicable, otherwise it should be deleted.)

- Independence of the ISSC

The ISSC acknowledges that it has carried out all of its duties independently and with the support and cooperation of the senior management and the Board of the Institution. The ISSC received the required assistance to access all documents and data, and to discuss all amendments and Shari’ah requirements. (Factors that have affected independence, if any, should be mentioned).

- The ISSC’s Opinion on the Shari’ah Compliance Status of the Institution

Premised on information and explanations that were provided to us with the aim of ascertaining compliance with Islamic Shari’ah, the ISSC has concluded with a reasonable level of confidence, that the Institution’s Activities are in compliance with Islamic Shari’ah, except for the incidents of non-compliance observed, as highlighted in the relevant reports. The ISSC also provided directions to take appropriate measure in this regard.

(Add a statement on any other breaches to the Shari’ah provisions, resolutions and controls established by the Higher Shari’ah authority, if applicable)

The ISSC formed its opinion, as outlined above, exclusively on the basis of information perused by the ISSC during the financial year.

Signatures of members of the Internal Shari’ah Supervision Committee of the Institution

Member’s Name Type of Membership Signature Member’s Name Type of Membership Signature Member’s Name Type of Membership Signature Member’s Name Type of Membership Signature Member’s Name Type of Membership Signature (End of the Template) - Responsibility of the ISSC

Guidance Note Re Charter of Internal Shari'ah Supervision Committee

N 5325/2020 Effective from 10/12/2020The Central Bank is pleased to attach herewith the Guidance Note Re Charter of Internal Shari’ah Supervision Committee, which applies to licensed financial institutions that conduct all or part of their activities and businesses in accordance with the provisions of Islamic Shari’ah (Islamic Financial Institutions).

This Guidance Note must be read in conjunction with the regulations, standards and resolutions issued by the Central Bank and the Higher Shari’ah Authority.

This Guidance Note is mandatory and effective from the date of this notice, taking into account what is stated in Article No. (4.2) of the Guidance Note.

Please bring this Guidance Note to the attention of the board of directors of your institution at the next board meeting.

Article (1) Introduction

- 1.1 This Guidance Note Re Charter of Internal Shari’ah Supervision Committee (“Guidance Note” or “Note”) complements the Standard Re Shari’ah Governance for licensed financial institutions that conduct all or part of their activities and businesses in accordance with the provisions of Islamic Shari’ah (“Islamic Financial Institutions” or “IFIs”) that was issued by the Central Bank (“Shari’ah Governance Standard” or “SGS”) with the aim to promote development of the banking system and to ensure its effectiveness and efficiency.

- 1.2. IFIs must establish Shari’ah governance policies and governance mechanisms to ascertain that the adopted Charter of Internal Shari’ah Supervision Committee (“Charter”) is compliant with requirements outlined in the Guidance Note and requirements outlined in the regulations, standards and resolutions issued by the Central Bank and the Higher Shari’ah Authority (“Regulations, Standards and Resolutions”).

- 1.3. Where the Guidance Note contains a stipulation (in an article) to provide information, or undertake certain measures, or address particular terms, as a minimum requirement, the Central Bank may impose (new) requirements additional to those specified in the relevant article (of the Guidance Note).

- 1.1 This Guidance Note Re Charter of Internal Shari’ah Supervision Committee (“Guidance Note” or “Note”) complements the Standard Re Shari’ah Governance for licensed financial institutions that conduct all or part of their activities and businesses in accordance with the provisions of Islamic Shari’ah (“Islamic Financial Institutions” or “IFIs”) that was issued by the Central Bank (“Shari’ah Governance Standard” or “SGS”) with the aim to promote development of the banking system and to ensure its effectiveness and efficiency.

Article (2) Objectives

- 2.1. The Guidance Note contains guidance aimed at facilitating implementation of requirements specified in the SGS related to establishment of the Charter.

- 2.2. The Guidance Note provides clarity on the supervisory expectations with respect to the Charter.

- 2.1. The Guidance Note contains guidance aimed at facilitating implementation of requirements specified in the SGS related to establishment of the Charter.

Article (3) Scope of Application

- 3.1. The Guidance Note applies to all IFIs.

- 3.2. The Guidance Note must be read in conjunction with the SGS and the standards and resolutions issued by HSA and notified to IFIs.

- 3.1. The Guidance Note applies to all IFIs.

Article (4) Compliance and Charter Template

- 4.1. Template of the Charter in Article No. 5 represents minimum requirement, and IFI may add additional paragraphs to its Charter provided such addition does not contradict requirements specified in the Regulations, Standards, and Resolutions.

- 4.2. The IFIs should comply with the Charter’s Template from 21 April 2021.

- 4.1. Template of the Charter in Article No. 5 represents minimum requirement, and IFI may add additional paragraphs to its Charter provided such addition does not contradict requirements specified in the Regulations, Standards, and Resolutions.

Article (5) Charter's Template

(template)

Charter for Internal Shari’ah Supervision Committee in (insert the name of the Islamic Financial Institution)

1. Introduction

- 1.1. This charter specifies the functional controls of Internal Shari’ah Supervision Committee of (insert the name of the Islamic Financial Institution) (“IFI”), and its meetings management, decision-making process, and other organizational matters (“Charter”).

2. Definition of Internal Shari'ah Supervision Committee

- 2.1. Internal Shari’ah Supervision Committee (“ISSC”) is a body, appointed by the IFI, comprised of scholars specialized in Islamic financial transactions, with the mandate to independently supervise transactions, activities, and products of the IFI and ensures they are compliant with Islamic Shari’ah in all its objectives, activities, operations, and code of conduct and other mandates stated in the relevant laws and standards.

3. Qualification of Members of ISSC

- 3.1. A member of the ISSC must meet the eligibility and competency requirements stipulated in the regulations, standards and resolutions issued by the Central Bank and the Higher Shar’ah Authority (“Regulations, Standards and Resolutions”).

4.Independence of the ISSC

- 4.1. It is mandatory to comply with the controls and guidelines specified in the Regulations, Standards and Resolutions to ascertain independence of the ISSC members.

5 Appointment of ISSC, Membership Period, Dismissal and Resignation of the Members

- 5.1. It is mandatory to adhere to the relevant standards regarding:

- appointment and formation of the ISSC,

- duration of the membership,

- dismissal or resignation of its members,

as specified in the Regulations, Standards and Resolutions. The ISSC should select from among its members a chairperson and a deputy chairperson in its first meeting.

- 5.1. It is mandatory to adhere to the relevant standards regarding:

6 Responsibilities and Authorities of the ISSC

- 6.1. It is mandatory to adhere to the standards regarding responsibilities of the ISSC stipulated in the Regulations, Standards and Resolutions.

7 The ISSC's Meetings and Issuance of Resolutions

- 7.1. The ISSC must meet regularly, at least four times in the fiscal year, and the period between two meetings should not exceed 120 days.

- 7.2. Quorum for ISSC meeting is constituted by presence of majority of its members. The ISSC resolutions are issued by the majority of its attending members, and in case of tied votes, the side with the chairperson prevails. The opinion of the member who is not in favour of the ISSC’s resolution must be recorded in the minutes of meeting with its reasoning.

- 7.3. Attendance of an ISSC member must not be less than 75% of the total meetings held during a year. An ISSC member may attend or convene the meeting in full through video or audio means of communication, if necessary, provided that this is recorded in the minutes of the meeting and approved by the ISSC members.

- 7.4. The ISSC may invite to its meeting the IFI’s directors, employees, experts, advisors, and other parties that ISSC decides in order to obtain clarification regarding data and information needed by ISSC in relation to the issues under their review. For the avoidance of doubt, the invitees are not entitled to vote on the ISSC’s resolutions.

- 7.5. The ISSC may issue resolutions by circulation in urgent cases, provided unanimity is reached. Resolution issued by circulation must be recorded in the minutes of the first meeting held after the issuance. In case of a disagreement, the ISSC should hold a meeting as soon as possible.

- 7.6. Resolutions of the ISSC must be:

- written in a clear form, and

- accompanied by procedures necessary for implementation of the provisions contained therein in a manner that ensures adequate execution. The ISSC specifies the details that must be accompanied with the resolution in relation to its implementation.

- 7.1. The ISSC must meet regularly, at least four times in the fiscal year, and the period between two meetings should not exceed 120 days.

8 Methodology of ISSC's Functions

- 8.1.a.The ISSC must thoroughly investigate matters on its agenda to establish adequate (fact-based) understanding related to nature of the presented matter. If a matter does not become clear to the ISSC, it may postpone issuance of the resolution or request additional information or supporting studies, and accordingly (in this case) the subject matter shall be presented again after the request is addressed.

- b.The IFIs must provide the ISSC with adequate time to:

- i.investigate the matters submitted to the ISSC, and

- ii.review any contracts and documents that may relate to the presented matters.

- b.The IFIs must provide the ISSC with adequate time to:

- 8.2.The ISSC should trace the Shari’ah ruling on the matter it is examining by:

- a.leveraging the legal opinions of Shari’ah jurists in the credible schools of law, and

- b.ensuring that the Shari’ah ruling does not contradict the Shari’ah standards or resolutions adopted by the HSA, even if such ruling differs from rulings issued by the ISSC in the past.

- 8.3.Fatwas issued by ISSCs of other institutions (i) are not binding on the IFI’s ISSC, and (ii) existence of those fatwas do not obviate the need for a resolution from the IFI’s ISSC, even if the members are same.

- 8.4.The resolutions of the ISSC are binding on its respective IFI in accordance with the applicable laws and standards.

- 8.5.The IFI must comply with interpretations of the ISSC regarding the HSA’s resolutions and standards or their implementation.

- 8.1.a.The ISSC must thoroughly investigate matters on its agenda to establish adequate (fact-based) understanding related to nature of the presented matter. If a matter does not become clear to the ISSC, it may postpone issuance of the resolution or request additional information or supporting studies, and accordingly (in this case) the subject matter shall be presented again after the request is addressed.

9 Subcommittees of the ISSC

- 9.1 To facilitate decision making process in urgent matters, the ISSC may choose to authorize:

- an executive member or

- an executive sub-committee,

from among its members, and determine their responsibilities.

Resolutions of the executive member or the executive sub-committee should be presented to the ISSC at its first meeting. Neither the executive member nor the executive committee has the right to issue a resolution on:- important transactions that contain new structures, mechanisms, or documentation that have not previously been endorsed by the ISSC (such as new structures, mechanisms and documentation in Sukuk issuances, syndicated financings or products), or

- to adopt plan of internal Shari’ah audit or endorsing reports submitted by the internal audit.

- 9.1 To facilitate decision making process in urgent matters, the ISSC may choose to authorize:

10 Internal Shari'ah Controls Functions

- 10.1 The IFIs must comply with the requirements related to Internal Shari’ah Control functions as stipulated in the Regulations, Standards and Resolutions.

11 Engagement (Appointment) Letter

- 11.1 An IFI must ensure that:

- the engagement letter by which a candidate is appointed to the ISSC conforms to the requirements specified in the Regulations, Standards and Resolutions,

- the candidate, whom the IFI wants to appoint to its ISSC, must have accepted content of the engagement letter before his/her name is submitted to the HSA and the General Assembly for approval, and

- the engagement letter must be available in Arabic.

- 11.1 An IFI must ensure that:

12 Approval, Effectiveness, Amendment and Review of the Charter

- 12.1 The Charter may be amended based on a request by the ISSC and approved by the board of directors, and the amendment will be effective from the date of its approval. The ISSC reviews the Charter at least once every two years or sooner if needed.

Approval of the Charter

Shaikh: Mr/Ms: Chairman of the ISSC Chairman of the Board ............................... ............................... Date of Signing: Date of Signing: Date of Approval: (Date of the latest signature above)

(end of the template)

Standard Re. Regulatory Requirements for Financial Institutions Housing an Islamic Window

N 4743/2020 STA Effective from 26/10/2020The Central Bank of UAE is pleased to attach herewith the Standard Re. Regulatory Requirements for Financial Institutions Housing an Islamic Window, which applies to licensed financial institutions that conduct part of their activities and businesses in accordance with the provisions of Islamic Shari’ah (Financial Institutions Housing an Islamic Window).

This Standard must be read in conjunction with the regulations, standards and resolutions issued by the Central Bank and the Higher Shari’ah Authority.

This Standard is mandatory and effective from the date of this notice, taking into account what is stated in Article No. (8) of the Standard.

Please bring this Standard to the attention of the board of directors of your institution at the next board meeting.

Article (1) Introduction

- 1.1 The Central Bank seeks to promote the development of banking activities to ensure their effectiveness and efficiency. To achieve this, licensed financial institutions that conduct part of their activities and businesses in accordance with the provisions of Islamic Shari’ah (“Institution housing an Islamic Window”) must establish a framework to ensure that the Shari’ah compliant activities and businesses are conducted in a manner that complies with the requirements set in this Standard and other Regulations and Standards issued by the Central Bank.

- 1.2 This Standard articulates the minimum requirements that Institutions housing an Islamic Window are required to comply with.

- 1.3 This Standard is issued pursuant to the powers vested in the Central Bank under the provisions of the Decretal Federal Law No. (14) of 2018 Regarding the Central Bank & Organization of Financial Institutions and Activities (the Central Bank Law).

- 1.4 Where this Standard specifies requirements to provide information, undertake certain measures, or address certain terms listed as a minimum, the Central Bank may impose requirements which are additional to those outlined in the relevant article.

- 1.1 The Central Bank seeks to promote the development of banking activities to ensure their effectiveness and efficiency. To achieve this, licensed financial institutions that conduct part of their activities and businesses in accordance with the provisions of Islamic Shari’ah (“Institution housing an Islamic Window”) must establish a framework to ensure that the Shari’ah compliant activities and businesses are conducted in a manner that complies with the requirements set in this Standard and other Regulations and Standards issued by the Central Bank.

Article (2) Objective

- 2.1 The objective of this Standard is to establish minimum requirements for the Shari’ah compliant activities and businesses of Institutions housing an Islamic Window, with a view to:

- Ensuring robust governance towards activities and businesses that comply with Islamic Shari’ah, and

- Contributing to financial stability and consumer protection.

- 2.2 This Standard elaborates on the supervisory expectations of the Central Bank with respect to Institutions housing an Islamic Window.

- 2.1 The objective of this Standard is to establish minimum requirements for the Shari’ah compliant activities and businesses of Institutions housing an Islamic Window, with a view to:

Article (3) Scope of Application

- 3.1 This Standard applies to all Institutions housing an Islamic Window. Institutions housing an Islamic Window established in the UAE with Group relationships, including Subsidiaries, Affiliates, or international branches, must ensure that the Standard is adhered to on a solo and Group-wide basis.

- 3.2 This Standard must be read in conjunction with the Standards and Resolutions issued by HSA and notified to Institutions housing an Islamic Window.

- 3.1 This Standard applies to all Institutions housing an Islamic Window. Institutions housing an Islamic Window established in the UAE with Group relationships, including Subsidiaries, Affiliates, or international branches, must ensure that the Standard is adhered to on a solo and Group-wide basis.

Article (4) Definitions

For the purposes of this Standard, the following words and phrases shall have the meanings stated below.

- a. Senior Management: The executive management of the Institution housing an Islamic Window responsible and accountable to the Board for the sound and prudent day-to-day management of the financial institution, generally including, but not limited to, the chief executive officer, chief financial officer, chief risk officer, and heads of the compliance and internal audit functions. The term Senior Management includes the head of Islamic banking at the Institutions housing an Islamic Window.

- b. Independence: Ensuring that the ISSC is not subject to any form of undue influence when issuing resolutions and fatwas in accordance with the Shari’ah parameters, and ensuring that the Internal Shari’ah Control Division or Section and Shari’ah Audit Division or Section are also not subject to any form of undue influence. This should be carried out to strengthen the confidence of both shareholders and stakeholders in the Institution housing an Islamic Window compliance with Islamic Shari’ah.

- c. Internal Shari’ah Audit: regular process to inspect and assess Institution housing an Islamic Window’s compliance with Islamic Shari’ah and the level of adequacy and effectiveness of the Institutions housing an Islamic Window’s Shari’ah governance systems.

- d. Compliance with Islamic Shari’ah refers to compliance with Islamic Shari’ah in accordance with:

a. resolutions, fatwas, regulations, and standards issued by the HSA in relation to licensed activities and businesses of Institutions housing an Islamic Window (“HSA’s Resolutions”), andb. resolutions and fatwas issued by ISSC (“ISSC”) of respective Institution housing an Islamic Window, in relation to licensed activities and businesses of such institution (“the Committee’s Resolutions”), provided they do not contradict HSA’s Resolutions.

- e. Shari’ah Supervision: monitoring of Institution housing an Islamic Window’s compliance with Islamic Shari’ah in all its objectives, activities, operations, and code of conduct.

- f. Subsidiary: An entity, owned by another entity by more than 50% of its capital, or under full control of that entity regarding the appointment of its board of directors.

- g. Affiliate: An entity owned by another entity by more than 25% and less than 50% of its capital.

- h. Fatwas: juristic opinions on any matter pertaining to Shari’ah issues in Islamic finance, issued by HSA or ISSC.

- i. Internal Shari’ah Supervision Division (or Section): a technical division (or section) in the Institution housing an Islamic Window with a mandate to support the ISSC in its mandate.

- j. Internal Shari’ah Supervisory Committee (“ISSC”): a body appointed by the Institution housing an Islamic Window, comprised of scholars specialized in Islamic financial transactions, which independently supervises transactions, activities, and products of the Institution housing an Islamic Window and ensures they are compliant with Islamic Shari’ah in all its relevant objectives, activities, operations, and code of conduct.

- k. Board: Institution housing an Islamic Window’s board of directors.

- l. Group: A group of entities which includes an entity (the ‘first entity’) and:

a. any Controlling Shareholder of the first entity;

b. any Subsidiary of the first entity or of any Controlling Shareholder of the first entity; and

c. any Affiliate, joint venture, sister company and other member of the Group. - m. Shari’ah Non-Compliance Risks: probability of financial loss or reputational risk that an Institution housing an Islamic Window might incur or suffer for not complying with Islamic Shari’ah.

- n. Confidential Information: information that is publicly unavailable and where its disclosure is not allowed as per Article 120 of Decretal Federal Law No. (14) of 2018.

- o. Higher Shari’ah Authority (HSA): is the Central Bank’s Higher Shari’ah Authority for Islamic banking and financial activities.

- p. Islamic Window: refers to the licensed activities that are carried on in accordance with the Islamic Shari’ah that are carried on by financial institutions whether for their account or for the account of or in partnership with third parties which comply with the regulatory requirements stated in this standard and other regulations issued by the central bank.

- q. High Quality Liquid Assets (HQLA): Assets unencumbered by liens and other restrictions on transfer which can be converted into cash easily and immediately, with little or no loss of value, including under the stress scenario.

- a. Senior Management: The executive management of the Institution housing an Islamic Window responsible and accountable to the Board for the sound and prudent day-to-day management of the financial institution, generally including, but not limited to, the chief executive officer, chief financial officer, chief risk officer, and heads of the compliance and internal audit functions. The term Senior Management includes the head of Islamic banking at the Institutions housing an Islamic Window.

Article (5) Governance Requirements

- 5.1 The Institution housing an Islamic Window must comply with Islamic Shari’ah in all of its goals, activities, operations and code of conduct in all matters related to Islamic window at all times.

- 5.2 Branches of foreign licensed financial institutions housing an Islamic Window must adhere to this standard or establish equivalent arrangements to ensure regulatory comparability and consistency. The equivalent arrangement, if applicable, should include the matters related to general assembly, the Board and its Committees without contradicting the prevailing laws in the UAE. The equivalent arrangements shall be submitted to the Central Bank for approval.

- 5.3 Each Institution with an Islamic Window is required to comply with the Shari’ah Governance Standard for Islamic Financial Institutions and other Regulations and Standards issued by the Central Bank, including but not limited to:

- a. The organizational structure of the Islamic window should ensure that the Shari’ah control divisions or sections are independent and are not subject to any influence that may affect their independence;

b. Alignment of the divisions or sections stated in the clause (a) with the three lines of defense approach as set out in the Central Bank’s Corporate Governance Standard and Shari’ah Governance Standard for Islamic financial institutions.

5.4 The Board is in ultimate control of the Institution housing an Islamic Window and accordingly responsible for the Islamic Window’s compliance with Islamic Shari’ah and the requirements set in this Standard.

5.5 Senior Management of the Institution with an Islamic Window is responsible and accountable to the Board for the sound and prudent day-to-day management of the Institution including executing and managing the Shari’ah compliant activities and businesses. All the Shari’ah compliant activities and business of the Institution must be offered through the Islamic window.

5.6 The Institution housing an Islamic Window should appoint a Head of Islamic Window who must be dedicated to the operations of the Islamic Window and must not perform any tasks that are not within the scope of the Islamic Window.

5.7 The appointment of the Head of Islamic Window must be approved by the Central Bank. The Central Bank must be informed regarding the organizational structure of the Islamic Window at least 20 working days before the same is implemented.

5.8 The Head of Islamic Window should report directly to the Executive Management Committee of the Institution or the CEO. The Head of Islamic Window is responsible and accountable to the Executive Management Committee of the Institution or the CEO for the operations of Shari’ah compliant activities and businesses. The Head of the Islamic Window is responsible to coordinate with the relevant departments concerning activities and businesses that comply with Islamic Shari’ah and shall be regarded part of the business line.

5.9 The Head of Islamic Window should:- have a bachelor degree or masters in banking and finance or other relevant fields,

- demonstrate adequate knowledge, and experience (not less than 10 years) in Islamic banking and finance that will allow him/her to lead Shari’ah compliant business, and

- have held relevant senior positions in the banking sector or other relevant sectors.

9.5 The Institution housing an Islamic Window must adopt an approach with regard to conducting the Shari’ah compliant businesses and activities within the institution. Such approach should take into consideration staffing and physical premises in accordance with the size and the complexity of the Shari’ah compliant business and activities. The approach may take one of the following forms:- -Stand-alone separate branches and offices to service the Islamic Banking clientele as well as designated staff;

- -Embedding of designated and/or dedicated Islamic Window personnel within the existing branch network and premises.

- -Any other form subject to the Central Bank approval.

Such approach must be approved by the ISSC and the approach submitted to the Central Bank for review and approval every 5 years unless the HSA or the Central Bank requires a shorter period.

- 5.10 The Institution Housing an Islamic Window may leverage on its existing infrastructure to source Shari’ah compliant activities, including the offering of Shari’ah compliant products and services through the existing business lines. The institution housing an Islamic Window must develop an approach to internal services (between different departments) with respect to Islamic Window in order to ensure the compliance with Islamic Shari’ah at all times.

- 5.11 The approach to internal services must include the following:

- a. A minimum of one designated function to manage Shari’ah compliant Asset and Liability Management (ALM), Treasury and Investment operations.

- b. A dedicated sales function with appropriate Shari’ah qualification to market and sell Shari’ah compliant products and services, and employees at this function are not allowed to market or sell conventional products. Other sales personnel may sell Shari’ah compliant financial products and services to customers provided that they have been given adequate and appropriate training and they are supported by the dedicated Islamic Window sales function.

- c. Development and delivery of a comprehensive and specific training plan to cover all staff engaged in Shari’ah compliant operations, including staff assuming positions in the front line, middle and back offices and control functions, to ensure adequate management of the Shari’ah compliant products and services within the institution. The training program should take into account:

- specifics of the functions (roles) performed by the staff, and equip the staff with information and skills, depending on the nature of work of each employee, to ascertain compliance with Islamic Shari’ah, and

- the general banking and business risks associated and encountered with that function as well as any Shari’ah non-compliance risks.

- d. The approach towards internal services should be approved by the ISSC and submitted to the Central Bank for review and approval. Any material changes thereafter must be submitted to the Central Bank for approval.

- 5.1 The Institution housing an Islamic Window must comply with Islamic Shari’ah in all of its goals, activities, operations and code of conduct in all matters related to Islamic window at all times.

Article (6) Asset and Liability Management

- 6.1 The institution housing an Islamic Window must establish an ALM Framework for the management of Shari’ah compliant assets and liabilities to ensure their sound and prudent management, including ring-fencing of Shari’ah compliant assets and liabilities.

- 6.2 The framework should demonstrate the segregation between Shari’ah compliant assets and liabilities and other assets and liabilities of the Institution.

- 6.3 The segregation must include having separate product codes for Shari’ah compliant products mapped with specific General Ledger accounts. Institution housing an Islamic Window may apply alternative methods, subject to the approval of the Central Bank.

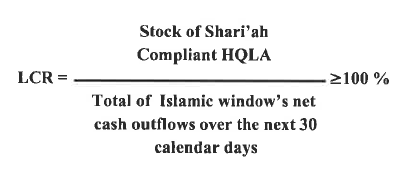

- 6.4 The Institution housing an Islamic Window is required to report a separate Liquidity Coverage Ratio (LCR)/Net Stable Funding Ratio (NSFR)/Eligible Liquid Assets Ratio (ELAR) (as applicable) for the Islamic Window. These reports are to be submitted along with periodic reports submitted to the Central Bank.

- 6.5 If the Institution housing an Islamic Window is maintaining separate liquidity levels for the Islamic Window, an appropriate stock of Shari’ah compliant High Quality Liquid Assets must be held against 30 days net outflow and documented accordingly for Central Bank supervision and examination review. Documentation must be retained for two years from any point in time that the information is documented

- 6.6 The formula of calculating LCR, specific to the Islamic Window operation is as follows:

6.7 Any surplus or deficit in Shari’ah compliant assets and liabilities in the Islamic Window must be managed in a Shari’ah compliant manner. Institutions must develop an approach to the mechanism of financing and funding between the Islamic window and the institution. The approach developed must be reviewed and approved by the ISSC and the Central Bank.

6.7 Any surplus or deficit in Shari’ah compliant assets and liabilities in the Islamic Window must be managed in a Shari’ah compliant manner. Institutions must develop an approach to the mechanism of financing and funding between the Islamic window and the institution. The approach developed must be reviewed and approved by the ISSC and the Central Bank.- 6.8 The management and treatment of non-Shari’ah compliant income shall be carried out in accordance with the directives of the ISSC.

- 6.9 Non-Shari’ah compliant income, if any, must be treated in accordance with the Shari’ah requirements in this regard.

- 6.10 There should be no internal procedure or a policy that encourages converting Shari’ah compliant assets to conventional assets. Similarly, the institution housing an Islamic Window must not transfer Shari’ah compliant assets (which are in the Islamic Window) to its conventional side in order to deal with it as a conventional asset. The Senior Management should ensure the independence of the Shari’ah compliance businesses and activities, and Islamic Window’s customers from the conventional businesses and activities.

- 6.11 All marketing and promotional material of Shari’ah compliant activities of the Bank must be formulated under a separate brand (e.g. different logo and different commercial name) and must be approved by the ISSC.

- 6.1 The institution housing an Islamic Window must establish an ALM Framework for the management of Shari’ah compliant assets and liabilities to ensure their sound and prudent management, including ring-fencing of Shari’ah compliant assets and liabilities.

Article (7) Regulatory and Financial Reporting, IT Systems and Infrastructure

- 7.1 The Institutions housing an Islamic Window are mandated to report a separate Islamic Bank Return Form “iBRF” as per the template set out by the Central Bank.

- 7.2 The Institutions housing an Islamic Window are required to separately report the results and activities of their Islamic Window to Executive Management and the Board. Such internal reporting shall include among other items an appropriate allocation of the costs of internal services to accurately reflect the cost of offering Shari’ah compliant financial services.

- 7.3 The reports produced by the Shari’ah control department or division and by the Shari’ah Audit department or division should be submitted in accordance with the requirements stated in the Shari’ah Governance Standard for Islamic Financial Institution.

- 7.4 The institution housing an Islamic Window are encouraged to separately report the results and activities of their Islamic Window operations within the annual report to promote market disclosure, transparency and customer confidence.

- 7.5The institution housing an Islamic Window may use a single or dual core banking system to record, manage and report Shari’ah compliant activities and other activities.

- 7.6 Where a single core banking system is used, it must be adjusted to account for the unique features of Shari’ah compliant products. Such adjustments for Shari’ah compliance purposes must be approved by the ISSC.

- 7.1 The Institutions housing an Islamic Window are mandated to report a separate Islamic Bank Return Form “iBRF” as per the template set out by the Central Bank.

Article (8) Compliance with the Standard

- 8.1 The Institutions housing an Islamic Window must set a Shari’ah governance framework in accordance with this Standard within 180 days from issuing this standard. The same must be submitted to the Central Bank for approval.

- 8.2 The Institutions housing an Islamic Window should comply fully with these standard requirements within one year from publishing this standard.

- 8.3 The Regulatory Development Division of the Central bank shall be the reference for interpretation of the provisions of this Standard.

- 8.1 The Institutions housing an Islamic Window must set a Shari’ah governance framework in accordance with this Standard within 180 days from issuing this standard. The same must be submitted to the Central Bank for approval.

Standard Re Shari’ah Compliance Function At Islamic Financial Institutions

Effective from 3/4/2025Article (1) Introduction

1.1 This Standard Re Shari’ah Compliance Function at Islamic Financial Institutions (“the Standard”)complements the Standard re Shari’ah Governance for Islamic Financial Institutions(“the Shari’ah Governance Standard” or “SGS”) with the aim to promote the development of the banking system and to ensure its effectiveness and efficiency.

1.2 The licensed financial institutions that conduct all or part of their activities and businesses in accordance with the provisions of Islamic Shari’ah (“Islamic Financial Institutions” or “IFIs”) must establish Shari’ah governance policies and governance mechanisms to ascertain compliance with requirements outlined in the Standard and requirements outlined in the relevant regulations, standards, resolutions and other notices issued by the Central Bank and by the Higher Shari’ah Authority (“HSA”) in relation to compliance with Islamic Shari’ah (“Regulatory Requirements”).

1.3 Where the Standard contains a requirement to provide information, or undertake certain measures, or address particular terms stated as a minimum requirement, the Central Bank may impose additional requirements to those specified in the relevant article in the Standard.

Article (2) Objective

The Standard sets supervisory expectations to implement the requirements specified in the SGS in relation to Shari’ah Compliance Function as part of the second line of defense.

Article (3) Scope of Application

3.1 The Standard applies to all Islamic Financial Institutions licensed by the Central Bank.

3.2 The Standard must be read in conjunction with the SGS and the standards and resolutions issued by HSA and notified to IFIs.

Article (4) Shari’ah Compliance Function

4.1 In accordance to Article No. (10.6) of the Shari’ah Governance Standard, the internal Shari’ah control division or section shall perform various functions, including Shari’ah Compliance Function (“SCF”). The SCF is responsible to continuously monitor compliance of an IFI’s businesses and activities with resolutions, fatwas, regulations, and standards, which are issued by the HSA.

4.2 The SCF is different from Shari’ah audit in terms of reporting line, frequency of the review, as well as the fact that SCF conducts reviews before and during the execution, while Shari’ah audit conducts review post execution.

4.3 The responsibility regarding managing Shari’ah Non-Compliance Risk lies with the IFI’s risk management department, not with the SCF. However, the two departments should provide each other with information in order to achieve compliance with Islamic Shari’ah and manage Shari’ah Non-Compliance Risk in a prudent manner.

Article (5) Stages of the Review Process in Shari’ah Compliance Function

5.1 The SCF shall conduct reviews and evaluate the Shari’ah Non-Compliance controls and their applications, issue reports on the same and monitor remedial actions to ensure that Shari’ah compliance controls are adequate and operate as intended.

5.2 The IFI must develop internal procedures and policies regarding SCF review exercises that should include, at least, the following stages: a. Develop an Annual Plan,

b. Planning and Scoping of the review,

c. Conduct a Field Review,

d. Documenting Issues & Actions,

e. Draft Reports, and

f. Monitor Progress.

The IFI may refer to the review stages that are stated in the Guidance Note of this Standard.

Article (6) Development of Annual Plan

The SCF shall be responsible for developing the annual review plan (“Annual Plan”) which must be approved by the Internal Shari’ah Supervision Committee (“ISSC”) and the Board.

Article (7) Planning and Scoping of the Review

The SCF shall set a planning and scoping of the review process (“Planning”), and it involves gathering information from the business or function under review, allowing development of the scope, objectives and approach to the review, and determining the planned review procedures.

Article (8) Field Review

The IFI’s SCF shall conduct a field review for the IFI that consists of procedures built on robust methodology basis. The details regarding field review may be referred to in the Guidance Note of this Standard.

Article (9) Issues and Actions

The SCF shall record each identified finding/incident in the report that follows every field review. The identified issues must be factual, accurate, precise, objective, clear, concise, complete and supported with:

a. Adequate evidence that demonstrates the accuracy and factuality of the identified finding.

b. Determination of the Shari’ah or governance or other documents and the relevant paragraphs from which deviation has occurred, if applicable, such as, but not limited to specific Regulatory Requirements, ISSC’s Resolutions, or the Products Manual.

c. Specification of the root cause that has triggered the identified finding.

d. Establishment of a clear action plan that adequately addresses the root cause and closes the gap, and specification of the party responsible for the action plan.

e. Specification of risk rating of the identified incident according to the approved risk matrix of the IFI which is prepared by risk management department.

Article (10) Reports

10.1 The SCF shall record the issues of the field review in a report that shall be developed through robust procedures before dissemination, as follows:

a. Preliminary Issues Report

b. Response from Respective Parties

c. Closing Meeting

d. Final Report

e. Final Report Approval

f. Final Report Dissemination

The IFI may refer to the detailed guidance in the Guidance Note of this Standard.

10.2 The final report shall be disseminated to the CEO and the relevant parties within five working days after being approved by the ISSC. This is to ensure the implementation of its contents within the period specified by the ISSC in the final report.

Article (11) Progress Status Monitoring

The SCF shall monitor progress updates provided by the relevant parties, and monitor the implementation of the action plan. The IFI may refer to the Guidance Note of this Standard for further guidance regarding the procedures that should adopted at this stage.

Article (12) Compliance with the standard

The IFI must comply fully with the requirements of this Standard within one year from its date of issuance.

Guidance Note Re Shari’Ah Compliance Function At Islamic Financial Institutions

Effective from 3/4/2025Article (1) Introduction

This Guidance Note Re Shari’ah Compliance Function at Islamic Financial Institutions (“Guidance Note” or “Note”) complements the Standard Re Shari’ah Compliance Function at Islamic Financial Institutions (“the Standard”) with the aim to promote the development of the banking system and to ensure its effectiveness and efficiency.

Article (2) Objective

The Guidance Note contains guidance aimed at facilitating implementation of the requirements related to Shari’ah Compliance at licensed financial institutions that conduct all or part of their activities and businesses in accordance with the provisions of Islamic Shari’ah (“Islamic Financial Institutions” or “IFIs”).

Article (3) Scope of Application

3.1 The Guidance Note applies to all IFIs. IFIs may comply with the guidance stated in this Guidance Note or apply equivalent criteria in order to comply with the requirements stated in the Standard. 3.2 The Guidance Note should be read in conjunction with the Standard and the standards and resolutions issued by Higher Shari’ah Authority (“HSA”) and notified to IFIs. Article (4) Development of Annual Plan

4.1 The Board and the senior management approve the Annual Plan that relate to Shari’ah Compliance Function (“SCF”) review exercises and ascertain smooth realization and implementation of the approved Annual Plan, including but not limited to, full cooperation and support from the relevant department heads at the IFI. 4.2 The IFI should prioritize what needs to be included in the Annual Plan, and develop a prioritization matrix that takes into account the relevant parameters, including: a. frequency of reviews, b. historical incidents, and c. size and complexity of products. Appendix (A) contains generic guidance on developing the prioritization matrix that aims to assist IFIs in identifying segments of operations and activities that should undergo review in a financial year. Article (5) Planning and Scoping of the Review

In the planning stage, the SCF should understand the regulatory requirements, the resolutions of Internal Shari’ah Supervision Committee(“ISSC Resolutions”) that relates to SCF, Shari’ah Non-Compliance (“SNC”) risks, compliance obligations, processes, policies and procedures, and related internal controls, including identifying and documenting known and self-identified issues. Subsequently, the SCF should send a memo outlining the reason for the review, scope, planned timeline and other terms of the scheduled review exercise to the relevant parties, including those departments or sections directly impacted by the review, prior to the commencement of the field review.

Article (6) Field Review

6.1 The Field Review May Include The Following

a. Opening Meeting, b. Sampling Methodology, c. Development of Internal Checklists, d. Walkthrough, e. Internal Controls Assessment, and f. Staff Awareness. 6.2 Opening Meeting

The SCF should start the field review with an opening meeting that involves representatives from the relevant departments and sections.

6.3 Sampling Methodology

a. The SCF should develop a sampling methodology that will be followed during the review exercise. The sample size and the sampling procedure should be objective and robust to ascertain with a high level of confidence that the selected sample fairly represents transactions executed during the period that is covered by the review exercise. b. The SCF should determine the sampling methodology which provides clarity related to the minimum quantity of samples that may be reviewed (such as 10% sample size) of the total number of transactions subject to the review exercise. Appendix (B) contains generic guidance for developing the sampling methodology. c. The SCF may need to select a larger or additional sample size than what was initially planned if the circumstances arise, such as in cases where there is reasonable uncertainty on whether an identified SNC incident/s is a random or systemic failure of the IFI to comply with the regulatory requirements and ISSC Resolutions. These instances should be specified in the IFI’s sampling methodology. 6.4 Development of Internal Checklists

a. SCF should develop checklists needed to undertake an adequate and effective review of the subject that is being reviewed. b. In developing checklists, the SCF should ascertain that it has mapped all requirements and expectations of the regulatory requirements and the ISSC’s Resolutions applicable to the subject planned to be reviewed, and that all relevant requirements are adequately transferred into the checklists. Appendix (C) outlines generic guidance for developing the respective checklists. 6.5 Walkthrough

a. SCF should conduct a walkthrough test of real-life deals to gauge the reliability of internal procedures, manuals and policies in relation to day-to-day activities of the IFI. b. The walkthrough should be accompanied by an assessment of the controls, their adequacy and effectiveness in real-life deals. Preparation for the walkthrough should include interviewing the relevant staff regarding the applicable processes and procedures, and questions or queries that would need to be asked during the walkthrough. The questions should cover exceptional and unusual situations that occur in day-to-day work. 6.6 Internal Controls Assessment

The SCF should assess internal controls related to SNC risk to ascertain their design and operational effectiveness. The assessment should, among others, cover the following aspects:

a. scope and adequacy of the control design in relation to addressing the SNC risk, b. operational reliability of the control and its effectiveness in identifying exceptions across all possible scenarios that could arise, c. probability of avoiding or circumventing the control, and d. comprehensiveness of the existing controls to address all relevant SNC risk. 6.7 Staff Awareness

a. The SCF should assess the staff awareness in relation to knowledge and skills that they need to possess to adequately fulfil their job duties, as per the responsibilities specified in the employee’s job description, without violating the provisions of Islamic Shari’ah. b. Determination of the type of knowledge and skills each employee needs to possess should depend on the nature of the employee’s responsibilities. For example, personnel with responsibility to execute the exchange of currency should be equipped with knowledge and skills specifically related to: 1. execution of all necessary steps or processes in currency exchange, which the employee is responsible for executing in line with parameters of Islamic Shari’ah. 2. reasonable understanding of SNC risks that may arise from this type of transaction, their potential consequences and steps or actions required to adequately manage the risks in order to prevent potential incidents from occurring. c. The IFI should develop proper training and staff awareness programme. Article (7) Issues and Actions

Article (9) of the Standard emphasizes that each identified finding/incident is included in the report. The SCF should analyze and identify the root cause and assess the following:

a. existence of reliable and efficient controls that should have prevented the identified incident from occurring, b. comprehensiveness and clarity of the internal policy’s requirement in relation to the incident, c. Whether the relevant employees are notified of, and have access to, the relevant internal policy, d. adequacy of staff awareness and the existing training programmes in relation to the identified finding, and e. staff conduct and adherence to the established policies, and potential conflict of interest. Article (8) Reports

8.1 Preliminary Issues Report

The SCF should send a report of preliminary issues (“Preliminary Issues Report”) to the relevant parties at least five (5) working days before the closing meeting.

8.2 Response from Respective Parties

After receiving the report, the respective parties should respond on the Preliminary Issues Report within a specific number of days. All responses should undergo an assessment by the SCF in light of the existing evidence related to the issue raised.

8.3 Closing Meeting

The SCF should conduct a closing meeting after completing the assessment of the responses. The relevant parties should be made aware of all the findings and supporting evidence. The meeting should be documented in the form of minutes of the meeting for audit purposes.

8.4 Final Report

a. The SCF when preparing the final review report (“Final Report”) should consider that the report is to assist the IFI in establishing effective and adequate procedures at the institutional level, making corrections and improvements where needed, and rectifying and closing identified gaps, if any. The Final Report should include: - adequacy of control status and adequacy of management action, - an executive summary that will briefly explain the scope and methodology used in preparing the report (such as specifying the total number of customers or transactions, sample size, list of issues and their risk grading, etc.), and - details of issues and actions as per the Standard and the Note. b. The Final Report may include a statement of the level of cooperation and support extended by the relevant departments to the SCF during the review exercise. 8.5 Final Report Approval

The SCF presents the Final Report, upon its completion, to the ISSC for assessment and approval. The ISSC should conduct a comprehensive assessment of the report regarding its compliance with the Standard, including but not limited to, assessment of the following aspects:

- validity of the identified issues, - accuracy of root cause/s of the issues and suitability of action plan, - adequacy and effectiveness of the controls, and - clarity of the report. The ISSC should maintain records of the same for audit purposes.

8.6 Final Report Dissemination

The SCF should conduct the following procedures regarding the Final Report Dissemination:

a. Circulating the final report to the relevant parties within five (5) working days after being approved by the ISSC. b. All findings of the report should be incorporated in the tracker for progress status monitoring (“Status Tracker”). c. Each party responsible for an action plan may confirm to SCF within the agreed timeline, or periodically if needed, that all the actions specified in the Final Report have been addressed, and substantiate such confirmation with adequate evidence for each finding. d. If any action from the Final Report is not closed/addressed within the timeline, the party responsible for the action plan should provide reasoning and evidences for not closing/addressing the issue, and its target completion date. e. The progress update on addressing the findings and implementing recommendations should be monitored. Article (9) Progress Status Monitoring

The SCF may consider the following procedures in the progress status monitoring, including but not limited to:

a. Monitoring progress updates provided by the relevant parties regarding how the findings are addressed and whether the action plan has been implemented. b. All responses should be supported with adequate evidence. The evidence should be kept for audit purposes. c. All responses received from the respective parties should be read in the context of existing evidence related to the highlighted issue. d. The Status Tracker should be updated based on the results of the monitoring. e. An update on the outstanding issues to be provided to the ISSC and risk management committee (or equivalent committee) in each meeting, and if needed, to the CEO of the IFI on a monthly basis for onward escalation in the relevant meetings. The update should be provided in a suitable format such as a dashboard that includes timeline analysis and is suitable for, and understandable by, each respective committee. f. Each party responsible for an action plan should seek approval from the ISSC, via SCF, for any extension to close the outstanding issue. Appendix (A): An Example in Prioritization Parameters for Selection of Subjects in the Annual Plan

1 Frequency of Reviews a. All products should be reviewed by the SCF at least once every three (3) years. b. All branches or distribution channels should be reviewed by the SC at least once every two (2) years. c. All new products should be reviewed within the first 3 months from the date when the product was launched. d. Products that have not been reviewed in the past are prioritized over those that have been reviewed. 2 Historical Incidents a. Products based on underlying contracts or concepts similar to those in which systemic or major incidents were identified in the past are prioritized over those in which no such incidents were identified. b. Distribution channels in which systemic or major incidents were identified in the past are prioritized over those in which no such incidents were identified. 3 Level of Complexity of the Products Products with higher level of complexity that negatively impact SNC risk are given priority over other products. Appendix (B): Generic Guidance for Developing Sampling Methodology

The selection methodology of the sample size should cover, among others, the following aspects: a. transactions of different sizes such as, small, medium and large transactions, b. transactions executed via different distribution channels and in different geographical areas, c. transactions executed with different customers, d. transactions executed in different currencies (if applicable), The selected transactions should be distributed throughout the period covered by the review exercise in accordance with the adopted methodology, such as equal distribution of samples across the period covered by the review exercise, or uneven distribution whereby transactions executed in certain periods may be deemed more vulnerable to the SNC risk and for that reason larger sample will be collected to ensure fair representation of the executed transactions in it during the time covered by the review. Appendix(C):Generic Guidance for Developing Product CheckList

Scope

Checklist for product review should cover all the relevant areas of a product that should be checked and their compliance with Islamic Shari’ah ascertained, including assessment of the following items: a. underlying structure of the product, b. templates of agreements, contracts, documentations, terms and conditions, (“Documentation Templates”) c. product related operational manuals, workflows, policies, guidelines, etc., (“Product Manuals”), d. relevant aspects of accounting entries/treatment, e. fees and charges, (if applicable), and f. compatibility of the IT system with Islamic Shari’ah in relation to operationalization of the product. The products should be reviewed by the SCF in accordance with a standard that considers the risks associated with the products. The SCF should review each product at least once every five (5) years. Aspects

Items specified in the Scope should be assessed from the below listed aspects (as applicable): a. Existence of well-maintained and complete record of all relevant and adequate ISSC’s approvals (and where applicable no objection letters from HSA or Central Bank) regarding Shari’ah compliance of the product prior to its launch, including approval of any amendments to the products before they are offered to the customers. b. Consistency of ISSC’s Resolutions with the regulatory requirements, which requires mapping details of the ISSC’s Resolutions regarding the product and their comparison with the regulatory requirements. c. Compliance of all items specified in the Scope with the regulatory requirements and ISSC’s Resolutions. This would include an assessment of the product details against the regulatory requirements and the ISSC’s Resolutions. d. Compliance of executed transactions with the regulatory requirements and the ISSC’s Resolutions. Standard Re External Shari’ah Audit for Islamic Financial Institutions

N 5785/2024 STA Effective from 29/11/2024Article (1) Introduction

The Central Bank seeks to promote development of the banking activities to ensure their effectiveness and efficiency. To achieve this, financial institutions that conduct all or part of their activities and businesses in accordance with the provisions of Islamic Shari`ah (“Islamic Financial Institutions” or “IFIs”) must comply with the requirements stated in this Standard when appointing a specialized external firm to conduct External Shari’ah Audit.

Article (2) Objective

The objective of this Standard is to set the minimum requirements that must be adhered for conducting an External Shari’ah Audit for the purpose of reassuring shareholders, depositors, and all stakeholders regarding the IFI’s compliance with Islamic Shari’ah Provisions.

Article (3) Scope of Application

3.1 This Standard applies to the IFIs in the case where:

- the IFI appoints an External Shari’ah Auditor on a voluntary basis, or - there is a regulatory requirement to appoint an External Shari’ah Auditor.

3.2 This Standard applies to all incorporated IFIs. IFIs established in the UAE with Group relationships, including Subsidiaries, Affiliates, or international branches, must ensure that the Standard is adhered to on a solo and Group-wide basis. 3.3 This Standard must be read in conjunction with the standards and resolutions issued by the Central Bank and the Higher Shari’ah Authority (“HSA”) and notified to IFIs. Article (4) Definitions

For the purposes of this Standard, the following words and phrases shall have the meanings stated below.

a. Senior Management: The executive management of the IFI responsible and accountable to the Board for the sound and prudent day-to-day management of the IFI, generally including, but not limited to, the chief executive officer, chief financial officer, chief risk officer, and heads of the compliance and internal audit functions. b. Internal Shari’ah Control Division (or Section): A technical division (or section) in the IFI that supports the ISSC in its mandate. c. Compliance with Islamic Shari’ah Provisions: It refers to compliance with Islamic Shari’ah in according with:

a. The provisions stated in Section Six of Book Three of the Commercial Transactions Law, b. The provisions contained in the bylaws issued implementing Section Six of Book Three of the Commercial Transactions Law, c. The resolutions, Fatwas, regulations and standards issued or adopted by the Higher Shari’ah Authority in relation to businesses and activities of the IFI ("HSA’s Resolutions"), d. The resolutions and Fatwas issued or approved by the Internal Shari’ah Supervision Committee of the respective IFI, in relation to businesses and activities of such IFI ("ISSC’s Resolutions"), provided that they do not contradict HSA’s Resolutions.

d. External Shari’ah Audit: An independent process to inspect and assess the IFI’s compliance with Islamic Shari’ah Provisions, and the level of adequacy and effectiveness of its Shari’ah governance systems for the relevant fiscal year, conducted by an external party. e. Internal Shari’ah Audit: The regular process to inspect and assess the IFI’s compliance with Islamic Shari’ah Provisions and the level of adequacy and effectiveness of IFI’s Shari’ah governance systems conducted by the Internal Shari’ah Audit division or department. f. Commercial Transactions Law: Federal Decree Law No. (50) of 2022 regarding the Commercial Transactions Law. g. Internal Shari’ah Supervision Committee (“ISSC”): A body appointed by an IFI, comprised of scholars specialized in Islamic financial transactions, which independently supervises transactions, activities, and products of the IFI and ensure its compliance with Islamic Shari’ah Provisions in all its objectives, activities, operations, and code of conduct. h. Board: Islamic Financial Institution’s board of directors. i. Shari’ah Non-Compliance Risks: Probability of financial loss or reputational risk that IFI might incur for not complying with Islamic Shari’ah Provisions. j. External Shari’ah Auditor: The Shari’ah audit firm and the individual audit engagement team members conducting the audit. Where relevant, specific references are made to the external Shari’ah audit firm only in certain paragraphs. k. Central Bank: The Central Bank of the United Arab Emirates. l. Islamic Financial Institutions (“Institutions/IFIs”): The Central Bank licensed financial Institutions that conduct all or part of their activities and businesses in accordance with the provisions of Islamic Shari’ah. m. Higher Shari’ah Authority: The authority established in accordance with the Decretal Federal Law No. (14) of 2018 Regarding the Central Bank & Organization of Financial Institutions and Activities, as amends. It exercises the mandates and responsibilities stipulated in the above mentioned decretal law. Article (5) Purpose of the External Shari’ah Audit

The purpose of the External Shari’ah Audit is to reach reasonable and independent assurance regarding the IFI’s Compliance with Islamic Shari’ah Provisions through an expression of an opinion thereon from the External Shari’ah Auditor.

Article (6) Basis of the External Shari’ah Audit

6.1 The External Shari’ah Auditor’s opinion must rely on the Shari’ah basis as per the order stated in Article (4/c). 6.2 If the External Shari’ah Auditor comes across an issue for which no provision is found in the list stated in Article (6.1), the External Shari’ah Auditor must refer to the IFI’s Internal Shari’ah Supervision Committee (ISSC) to obtain a Shari’ah resolution for the same. Article (7) Fit and Proper

7.1 To conduct External Shari’ah Audit for IFIs, the external Shari’ah audit firm must be approved by the Central Bank. The firm will be granted the Central Bank approval after fulfilling certain criteria, including that the firm must have:

a. a license issued by competent authorities to perform its business in the UAE, b. at least three years of experience in Shari’ah audit. As for new firms, the approval may be granted to such external Shari’ah audit firms under special conditions that enable them to gain experience in External Shari’ah Audit, c. adequate resources to conduct the duties of External Shari’ah Audit and disclose the names of personnel specialized in Shari’ah audit engaged by the firm, d. an External Shari’ah Audit team that meets the competencies required to carry out External Shari’ah Audit duties. These include Shari’ah proficiency, accounting and legal experience, and other competencies according to the nature of the IFI’s business. In all cases, the personnel specialized in Shari’ah audit who meet the conditions stipulated in Article (7.3) must not be less than two-thirds of the team members, e. formal manual that states its methodology in conducting External Shari’ah Audit’s duties. The manual should be in line with the best practices in this field.

7.2 Firms that conduct external audit and are not specialized in External Shari’ah Audit may perform External Shari’ah Audit as long as they meet the criteria stipulated in this Standard and they must be approved by the Central Bank. 7.3 Personnel specialized in Shari’ah audit must fulfil the following conditions:

a. Should have a university degree in Islamic Shari’ah or relevant specializations, b. Should have a professional certificate in Shari’ah Auditing such as certificates issued by the Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) or the General Council for Islamic Banks and Financial Institutions (CIBAFI), c. Should have sufficient expertise of at least seven years in Shari’ah Audit, d. Proficiency in Arabic and English, e. Should not be sentenced by a final decision in crimes related to honor or honesty, or convicted of offences and sentenced by imprisonment. Article (8) Appointment of External Shari’ah Auditor