Regulation No. 29/2011 Regarding Bank Loans & Other Services Offered to Individual Customers

C 29/2011 Effective from 23/3/2011This regulation has been amended and clarified by the following notices respectively (E 28/02/2011), (N 2705/2012), (N 4501/2011), (N 13/1187/2013), (N 22/2017), (N 193/2018), (N 3986/2019), (N 5060/2019) and (N 2535/2022). You are viewing the latest version. Please find the PDF of the previous version on the table below.version 2 (consolidated as of 24/06/2022) pdf download version 1 (effective from 23/03/2011) pdf download Introduction

Following review of reports on loans and other services offered to individual customers, and banks' responses to the questionnaire previously sent, titled "Personal Consumer Loans", and pursuant to provisions of article nos. (5), (18), (94) and (96) of Union Law No (10) of 1980, Regarding the Central Bank, the Monetary System & Organization of Banking, the Central Bank has decided that all banks must abide by the provisions of these regulations, at all times.

Objective

The objective of these regulations is to determine the relationship between banks (conventional and Islamic) and finance companies on the one hand, and their individual customers on the other, in a more transparent manner, so as to boost confidence in banks and finance companies and enhance credibility of the banking system.

Article (1) Definitions

a) Bank Transfer: Transferring funds electronically from one account to another, whether inside the UAE or to an account abroad.

b) Bank's Cheque: A manager's cheque, or a cheque where the bank is the drawer and the beneficiary is an individual, an establishment, a commercial company or a government institution, inside or outside the UAE.

c) Bank Guarantees: Guarantees issued by banks on behalf of their customers (including retail customers), which are usually payable upon first demand by the beneficiary.

d) Debit Cards: Cards similar to credit cards, except that purchases and withdrawals charged to it are immediately deductible from the account.

e) Prepaid Cards: Cards filled with value, where purchases and withdrawals are deducted from the stored value until depleted (or fully exhausted).

f) Top-Up Loan: An additional loan obtained by the borrower from the lending bank or finance company, prior to full repayment of the outstanding loan.

g) Commissions: Rates charged against particular banking services rendered by banks.

h) Fees: Rates charged against particular banking services, commitments or obligations.

i) Deductions: deductions or debits to bank accounts against banking services.

j) Deductible Charges: Charges to accounts against banking services.

Article (2) Personal Loan

a) Personal Loan: Is "a loan that is given to individual customers, where repayments are made out of salary and end of service indemnity and/or any other verifiable regular income from a well-defined source".

b) Personal Loan's Limit: Amount of the personal consumer loan has been set at (20) twenty times the salary or the total income of the borrower, and banks and finance companies must make sure that this limit is not exceeded.

c) Repayment Period: The repayment period for this loan must not exceed (48) months.

d) In order to ensure that the monthly installments deducted for repayment of this loan and resulting interest are kept in a reasonable proportion to the customer’s income, the deductions from his salary and/or regular income must not exceed the limits specified under Article (7) of these Regulations.

e) Loans extended to sole proprietorship firms and companies, secured by salary of the owner or salaries of the partners shall be treated the same way this loan is treated, and shall be subject to the same terms and conditions.

f) This loan shall be extended as per an application by the customer to be approved by the bank or the finance company, and it should be drafted in the manner set out in Article (12) hereof.

Clarifications and Guidelines (Notice No. 2901/2011)- These regulations apply to personal facilities viz. loans, overdrafts, car loans and credit cards extended to individuals which are repayable from salary, end of service indemnity and/ or other verifiable regular income from a well defined source.

- It should be ensured that the borrowers’ salary and end of service benefits are properly ascertained from the employer. If the facility is partly or fully given against other income, it should be from a well defined source and its full details should be obtained.

- In case of borrowers with heavy personal commitments and lower disposable income or uncertain employment/ job prospects, banks may not allow facilities up to the upper limit of 20 times salary and/ or the total income, repayable within 48 months despite meeting the specified criteria.

- .For sound loan decisions, banks should have clear policy guidelines on issues which have direct bearing on the quality of risk and repayment of the loan.

- If a customer avails for a lower amount than his eligibility or there is significant increase in his income level in subsequent months due to promotion etc, banks may reassess his eligibility after proper verification. In such a case, either existing loan is enhanced or a new loan is set up (without disturbing the existing loan).

- If other income is main or supplementary source of repayment, it should be ensured that such income is from a known regular source, the borrower has produced documentary evidence of such income.

- Besides personal facilities against salary and other income as above, banks may extend loans and overdrafts against lien over fixed deposits held with them.

Article (3) Car Loan

a) Car Loan: Is a loan extended by the bank or the finance company to its customer for the purpose of purchasing a private car.

b) Car loan shall be treated as separate from the personal consumer loan, and should not exceed (80%) eighty percent of the value of the financed vehicle.

c) Repayment Period: The maximum period for repayment of the loan shall be (60) months.

d) Security: This loan should be secured by a mortgage over the car.

e) Car loans extended to sole proprietorship firms and companies, secured by salary of the owner or salaries of the partners shall be treated the same way this loan is treated, and shall be subject to the same terms and conditions.

f) This loan shall be extended as per an application by the customer and approved by the bank or the finance company, and it should be drafted in the manner set out in Article (12) of these Regulations.

Clarifications and Guidelines (Notice No. 2901/2011)- Banks may finance passenger new and used cars to the extent of 80% of their value. Financing of commercial vehicles is outside the purview of these regulations unless repayment of the loan is from the salary of the customer and other laid down criteria are satisfied.

- Financing of operating leases to individuals would not be considered as car finance and would not fall within these regulations.

- Car loans may be allowed in addition to the personal loan as above but within the 50% of gross salary and any regular income as explained in Article (7).

Article (4) Overdraft Facilities

a) Overdrafts: Are "facilities linked to customers accounts, and are provided by banks for payment on their behalf, in advance. This usually results in a negative balance in the customers' accounts, which would require deposit of funds to cover that balance plus resulting interest and deductions".

b) Overdraft facilities extended to sole proprietorship firms and companies, secured by salary of the owner or salaries of the partners shall be treated the same way these facilities are treated, and shall be subject to the same terms and conditions

c) To obtain such facilities, there should be pre-arrangements between the customer and the bank. The customer must submit his application, which shows the purpose of the facilities, the expected repayment period and the sources of repayment, in accordance with the form set out in Article (12) of these Regulations.

Clarifications and Guidelines (Notice No. 2901/2011)- Overdrafts limits will be counted within 20 times salary as specified for the personal loans under Article (2) above

- Islamic banks may allow overdraft facilities by whatever name described in accordance with Shariaah principles, without violating the upper limits and other requirements of these regulations.

Article (5) Credit Cards

a) Credit Cards: Are "Plastic cards linked to an electronic network, containing details and credit limit of the card holder. Value of a customer's purchases and cash withdrawals are paid on his behalf by the issuing bank or the finance company, and the customer pays the value at the beginning of the month following the transactions' month, or by installments as per agreement with the issuing bank or finance company, after end of the period allowed for full payment of the balance.

b) Credit cards shall be issued to customers of the bank or the finance company, and may be issued to non-customers, in which case customer statistical data, as residents or non-residents, must be recorded separately.

c) Banks and finance companies issuing such cards must abide by the following:

1. Provide these cards to persons whose annual income equal or exceeds AED 60,000.

2. These cards may be provided against a pledged deposit of value not less than AED 60,000.

d) Banks or finance companies should provide their credit card customers with a monthly statement of expenses, showing values of purchases and cash withdrawals, and they should immediately investigate if a customer challenges any expense item.

e) Credit card facilities for the unpaid balances of these cards provided to sole proprietorship firms and companies and secured by salary of the owner or salaries of the partners shall be treated the same way these facilities are treated, and shall be subject to the same terms and conditions.

f) Provisions of the agreement for providing credit cards, signed by the customer, should be in accordance with the form set forth in Article (12) of these Regulations.

Clarifications and Guidelines (Notice No. 2901/2011)- In order to ensure that credit cards are issued to creditworthy individuals, a mandatory minimum income level of AED 60,000 per annum has been stipulated. Banks may fix the limits within the policy as stated in this regulation.

- Those not meeting the above income criteria are required to place a pledged deposit of not less than AED 60,000 with the bank for issuance of credit card. However such persons may be permitted credit facility besides credit card provided aggregate of credit facility and credit card limit do not exceed 50% of the pledged deposit.

- Credit card limit is allowed as additional facility but repayment of outstandings must remain within 50% of gross salary and any regular income as explained in Article (7).

- Banks may encourage greater use of debit cards for the customers who are not found to be eligible for issuance of credit card.

- If the cards have been issued to non-customers, banks should compile statistical data separately for residents and non-residents and review them from time to time.

- Banks will take particular care in respect of credit cards issued to non-residents.

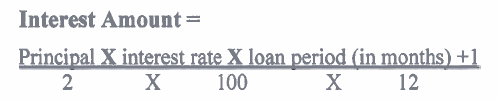

Article (6) Interest

Computation of Interest

a) Each bank or finance company must calculate the interest rate charged for the loans mentioned under article nos. (2) and (3) and overdraft facilities (Article- 4 in case of banks only) as well as unpaid credit card balances (Article -5), in accordance with the following formula:

b) All banks and finance companies must declare their respective interest rates on loans, overdraft balances (In case of banks only), and balances due for credit cards within the table. The rate shall be determined on basis of the reducing balance of the loan on annual basis and included in the display board mentioned in Article (11) of these Regulations.

c) "Interest Amount" on loans and overdraft balances shall be determined on basis of the formula mentioned under (a) above.

d) Deduction of a ratio of the loan in advance, as the payable interest amount is prohibited, the formula mentioned under (a) above should be used to calculate the first interest amount, and then interest amount shall be calculated on the reducing balance of the loan by using the following simple equation:

e) Banks and finance companies must arrive at the "Interest Amount" and deduct it from the agreed monthly installment, then use the net amount to reduce the loan balance and reach "the new balance of the loan at the beginning of the month" which would, in turn, be used in the calculation process at the end of the following month.

f) With regard to calculation of interest amount on credit cards due balances, these shall only be calculated for the outstanding balance after the maturity date for its full payment; i.e., in the month following the month on which the purchases and withdrawals have occurred. Interest amount must then be calculated as per the equation mentioned under (a) above and in accordance with the rates declared on the display board mentioned under Article (11) of these Regulations.

g) A Bank or a finance company shall determine the penalty rate in the event of full or partial prepayment before maturity date, or in case of a top- up loan, however, a top- up loan, should not be granted unless the original loan was repaid, without default, for a period not less than one year, and in this case the rate shall be declared in the table mentioned in Annex-2

Clarifications and Guidelines (Notice No. 2901/2011)- Method of interest calculation has not been changed from the earlier Circular No 12/93. Banks should continue to follow reducing balance method, by taking a year of 365 days. However they must ensure that effective interest rate on per annum basis is disclosed to the customer, displayed on the Board, it is used for calculation and specified in the loan documentation.

- .While reducing balance method of interest calculation will be followed on personal and car loans, average daily outstanding balances will form the basis for interest calculation in all cases.

- In case of credit cards, the banks may continue to follow the global practice where no interest/ finance charges are levied on the outstanding balance (excluding cash advance transactions) when the new balance outstanding shown in the statement is paid in full by the Payment Due Date. Finance/ interest charges on cash advance may be applied from the transaction date till final repayment.

- Within the above broad framework, Islamic banks may vary display of interest rates or use appropriate terminology as permitted under the Shariaah.

- Any bank advertising or propagating ‘Flat’ interest rate must invariably state the equivalent effective rate side by side.

Article (7) Repayment Installments

a) Deductions from salary or regular income of any borrower, for all types of loans extended by banks and finance companies together, including, but not necessarily restricted to, car and private housing loans, overdraft facilities, and credit cards facilities, must not exceed 50% fifty percent of his gross salary, and any regular income from a defined and specific source at any time.

b) Should a loan or a banking facility's repayment period extends to the retirement age, banks and finance companies must schedule reduction of these loans or facilities in such way as to allow deduction of only 30% of the income (or pension salary).

c) Banks and finance companies may only take from the customer the number of postdated cheques covering the installments, and of value not exceeding 120% of value of the loan or the debit balance.

Clarifications and Guidelines (Notice No. 2901/2011)- All the lenders are obliged to carry out proper due diligence to ascertain the applicants’ liabilities and income sources so that total installments including payments on account of credit card do not exceed 50% of their gross salary and other regular income.

- Personal loans will be setup for a maximum tenor of 48 months. However if a borrower retires before full repayment, his loan will be restructured from the date of retirement so that his total repayments do not exceed 30% of income (or pension salary).

- Existing loans will continue in accordance with the present arrangement and documentation. However no top ups, deferrals or rescheduling will be permitted beyond eligibility in terms of salary multiplier, tenor and repayment percentage.

- Banks should formulate specific policy on top ups and rescheduling in order to restrict their frequency. It should be ensured that there is no ‘ever greening’ of loans to disguise problem or delinquent loans.

- In case of Islamic banks, they have to ensure that in case of prepayment, adequate rebate is allowed to a customer so that final charge to him does not exceed the level given in Annexure 2 to the Circular.

Banks are permitted to defer up to two instalments in a year at their discretion. (NOTICE NO. 4501/2011)

Article (8) Armed Forces Staff Loans

In the case of army personnel, the conditions detailed in our Notice No. 1850/2004 dated 14/06/2004 shall continue to apply, but with the following amendments:

a) The value of installments deducted by the bank (or the finance company) for all types of loans and facilities (personal- commercial- housing – car loan- credit cards and any other loans or facilities) shall not exceed 50% of the borrower's gross salary.

b) Military ID cards should not be taken, nor photocopied. A certificate issued by the Armed Forces stating gross salary, period of service and that the applicant is still holding his job should suffice.

c) In case a lending bank or finance company fails to abide with the above, the Armed Forces shall transfer the salary of the concerned Armed Forces staff to any other bank (or finance company) without referring to the bank that extended the loans or facilities.

Article (9) Bank Accounts & Related Commissions, Fees and Charges

a) Bank Accounts are: current accounts, savings accounts, call accounts and the like, as well as accounts set-up for specific purposes.

b) Commercial banks may open all types of accounts for their retail customers, but in such cases, they must abide by the standard agreement mentioned under Article (12) of these Regulations. In case a customer requested closing of the account and termination of the business relationship with the bank, the bank should do that without imposing a penalty if the account opening date goes back to more than one year. In all cases, an account must be closed and an appropriate certificate must be issued within, maximum, seven days (7) from date of submission of the application.

c) Banks may set a minimum credit balance for each account, and impose charges if such minimum was not maintained, as specified in Article (11) of this regulation.

d) None of the opened accounts can be considered "dormant" if the customer's address is known or if the customer is present and has other active accounts with the bank. Accounts are classified as dormant only in accordance with the provisions of these regulations issued by the Central Bank in this regard.

e) Banks may issue ATM cards, or debit cards linked to any type of these accounts. They may also charge fees for issuance of new cards, replacement of lost cards or renewal of expired cards. However, they must declare these fees in the manner specified in Article (11) of these Regulations.

Clarifications and Guidelines (Notice No. 2901/2011)- Banks may continue with their present practices and internal guidelines to control and monitor dormant accounts. However in no case they should transfer the balance of such accounts to their profit and loss account.

- Central Bank is in the process of issuing suitable guidelines in respect of dormant accounts. In the interim, banks may continue to comply with Notice No 24/2000 in respect of dormant accounts and take necessary precautions for operating such accounts.

Article (10) Personal Banking Services & the Fees and Commissions Charged on them

a) Personal Banking Services: are bank transfers, issuance of bank cheques (or manager's cheques) issuance of bank guarantees, opening of documentary credit, discount of cheques of local and foreign banks, issuance of balance certificates, issuance of indebtedness certificates and the like.

b) All banks and finance companies (finance companies are not permitted to open current, savings or call accounts to retail customers or provide services and facilities relating to such accounts) may provide the personal banking services mentioned in (a) above and collect related commissions and fees, or deduct such fees from the account, however they should declare them in the manner specified in Article (11) of these Regulations.

Clarifications and Guidelines (Notice No. 2901/2011)- Relevant fees, charges and commissions applicable to personal customers have been specified in the Appendices to the Circular. Banks are not allowed to levy any other commissions, fees, charges or fines without Central Bank’s written approval. Banks are however free to reduce or exempt their customers from payment of certain fees and charges at their discretion.

- Loans and insurance are separate products. Hence it should be a customer’s choice to select either to pay them together over the period of loan or to pay upfront. Banks should however explain to the customer properly and obtain his concurrence before charging him for the insurance.

- List of charges and commissions apply to personal loans, car loans and personal overdrafts. Banks may continue to levy charges and commissions on credit cards as hitherto as no change has been proposed in the regulations.

- If there are other important fees and charges applicable to certain segment of customers but left out in the Appendices, these may be submitted for consideration of the Central Bank.

Article (11) Interest Rates, Commissions and Banking Service Charges

a) Each bank or finance company shall determine the interest rates pertaining to personal loans and car loans (must include insurance and expressed in one figure) along with overdraft balances and unpaid credit cards balances and include them in the table shown in Annex-1 of these Regulations. Copy of this table must be sent for publication by the Central Bank.

b) Fees, commissions, deductions and charges on loans, overdraft balances and unpaid credit card balances and those charged on retail banking services, shall be in accordance with the limits prescribed in the table shown in Annex-2 of these Regulations. Banks and finance companies may not impose any commissions, fees, charges or fines other than those mentioned in the said table without Central Bank's written approval.

c) Any Fees/commissions on purchase/sale of currency notes, Travelers Cheques, Demand Drafts, and Telegraphic Transfers for major countries must also be clearly written in Arabic and English on a board of an appropriate size to be fixed next to the Foreign Exchange Counter in the banking hall at banks’ branches, as shown in Annex-3 of these Regulations.

d) The Central Bank shall annually review fees, commissions and charges imposed as per table No-(2) attached to these regulations.

Clarifications and Guidelines (Notice No. 2901/2011)- Relevant fees, charges and commissions applicable to personal customers have been specified in the Appendices to the Circular. Banks are not allowed to levy any other commissions, fees, charges or fines without Central Bank’s written approval. Banks are however free to reduce or exempt their customers from payment of certain fees and charges at their discretion.

- Loans and insurance are separate products. Hence it should be a customer’s choice to select either to pay them together over the period of loan or to pay upfront. Banks should however explain to the customer properly and obtain his concurrence before charging him for the insurance.

- List of charges and commissions apply to personal loans, car loans and personal overdrafts. Banks may continue to levy charges and commissions on credit cards as hitherto as no change has been proposed in the regulations.

- If there are other important fees and charges applicable to certain segment of customers but left out in the Appendices, these may be submitted for consideration of the Central Bank.

Article (12) Conditions for Opening of Accounts, Providing of Credit Cards and Granting Loans & Bank Facilities

a) Conditions for opening of accounts of all types as well as conditions for obtaining credits cards must be included in a standard agreement, drafted in both English and Arabic and written in an easily readable font, and in accordance with texts drafted and approved by the Emirates Banks Association.

b) Conditions for granting personal loans, car loans, overdraft facilities and facilities for covering unpaid credit card balances must be included in standard applications, drafted in both Arabic and English and written in an easily readable font, and in accordance with texts drafted and approved by the Emirates Banks Association.

Clarifications and Guidelines (Notice No. 2901/2011)- Emirates Banks Association will be providing the banks with standard account opening forms including general terms and conditions and other loan documentation which will be beneficial to various user groups. Pending finalization and introduction of new forms, the banks may continue to use the existing forms as hitherto.

- In addition to the above, each bank will also be allowed to define specific terms and conditions which do not require prior approval from the Emirates Banks Association or Central Bank provided these are signed by the customer and do not contravene or contradict any other requirement. These terms will be shown in a separate section along with general terms and conditions.

Article (13) Shariaah Compliant Banking Services

The provisions of these Regulations shall apply to Shariaah compliant banking services, except in the matter of computing interest and determining its amount, which would be done in accordance with Shariaah principles.

In such case, clarity, transparent disclosure, accuracy and documentation at all times, must all be observed, and copy of the established rates should be sent to the Central Bank for publication.

Clarifications and Guidelines (Notice No. 2901/2011)Islamic banks will be allowed to use certain special terms applicable only to such banks, viz profit, finance, etc. However scheduled rates under different names or descriptions should be in accordance with these regulations and sent to Central Bank for information and publication.

Article (14) Violations to the Provisions of These Regulations

Should suspicions arise as to the violation of provisions of these Regulations by any bank, the matter shall be referred to the Legal Development Unit of the Central Bank to decide whether such violation has occurred. If the violation is established, the fine referred to in Article (107) of Union Law No-(10) of 1980 Regarding the Central Bank, the Monetary System and Organization of Banking, shall be imposed, and shall apply to each violation, and be charged on daily basis to the violating bank, until rectified.

Article (15) General Provisions

a) Banks or finance companies are not allowed to alter or vary terms and conditions for granting the loan or the facility during the tenor of the loan or the facility, unless agreed to in writing by the borrower. In case of changes to the commissions or fees, customers must be notified, at least, two months prior to implementation of such changes.

b) Banks and finance companies are prohibited from taking blank cheques for granting loans or overdraft facilities, or for issuing credit cards.

Clarifications and Guidelines (Notice No. 2901/2011)- If a bank uses additional pages to the forms prescribed by the Emirates Banks Association, such sheets containing terms and conditions should be accepted by the borrower under his signature.

- Banks are not expected to upgrade a customer’s status whether for his credit card or other similar facility unless his prior concurrence has been obtained. Besides written concurrence, banks would be allowed to use SMS or email facility to communicate with the customers and obtain their concurrence.

- Effective 1 May, 2011 all new personal accounts will be subject to the revised fee structure. Existing customers will however be given two months notice from that date through letters or via electronic means. Further the revised fee and charges will not be applied retrospectively.

- Banks should continue to pay greater emphasis on cash flow/ repaying capacity of the borrower and less on security or guarantee.

- 5.As hitherto, banks are prohibited to take private houses as security for personal loans or take personal guarantees as security when these loans are given to non-UAE nationals.

- No fees and charges have been mentioned for credit cards and banks may maintain status quo.

- Banks may levy relationship based fee on personal accounts and offer incentives to high value customers provided a specific fee or charge does not exceed the maximum permissible rate specified in the rate structure.

Article (16) The Provisions of These Regulations are not Applicable to Merchant and Investment Banks

The provisions of these Regulations are not applicable to investment banks or merchant banks, nor to finance or investment companies, since these institutions are not authorized to provide personal loans or retail banking services. Moneychangers, however, shall only be subject to the provisions regarding bank transfers and exchange of currency.

Article (17) Responsibilities of the Banking Supervision & Examination Department

a) The Banking Supervision & Examination Department will issue a guide to clarify how banks should comply with the provisions of these Regulations and submit the required statistical data to the Central Bank.

b) The Banking Supervision & Examination Department will also issue a guide to its examiners to explain the regulatory procedures relevant to these Regulations.

Article (18) Cancellation of the Previous Circular on the Subject

Upon enforcement of this Regulation, Circular No- 12/93 dated 23/2/1993, and Central Bank's clarifications ref. DMM/1263/93 dated 6/7/1993, and any notices or directives relating thereto shall be cancelled, except for Notice No- 1850/2004, dated 14/6/2004, regarding Armed Forces Personnel.

Article (19) Interpretation of These Regulations

The Legal Development Unit of the Central Bank shall be the reference for interpretation of the provisions these Regulations.

Article (20) Currently Outstanding Loans

a- The provisions of these Regulations shall apply to all banks and finance companies including Islamic banks and Islamic finance companies in relation to personal consumer loans and car loans granted by these entities currently existing, except for commissions, fees or any fines charged on them prior to the date on which these regulations come into force, which is considered finalized.

b- Any borrower may transfer his/her loan/financing from any bank or finance company operating in the UAE against paying of an early payment fee not exceeding 1% of the outstanding balance of the loan, or AED 10,000, whichever is less. Another bank or a finance company operating in the UAE may accept the transfer under the following conditions:

- For loans granted after the issuance of this Regulation, the requirements of the Regulation must be fully complied with, in particular those relating to the loan or financing amount, the repayment period and monthly deduction.

- For loans granted prior to the issuance of this Regulation, the profit/interest rate should be reduced and the repayment period or loan/financing balance should not be increased by granting an additional loan or financing to the borrower.

Clarifications and Guidelines (as per Notice No. 2901/2011)- Existing loans and overdrafts will continue to be governed by the terms and conditions agreed between the parties. However early settlement charges, other charges, fees and commissions levied after 1st May, 2011 will be in accordance with the new structure.

- New loans extended after 1st May, 2011 or rescheduled after that date will be subject to the new regulations.

- In exceptional circumstances such as rescheduling due to retirement of the borrower or loss of his income for any other reason, a longer repayment period beyond 48 months could be permitted.

- For loans granted after the issuance of this Regulation, the requirements of the Regulation must be fully complied with, in particular those relating to the loan or financing amount, the repayment period and monthly deduction.

Article (21) Publication

These regulations shall be published in the Official Gazette in both Arabic and English, and shall come into effect one month after date of its publication.

Appendix No. (1)

Interest rates charge on Loans

Interest Rate Range Interest/profit on a personal loan (p.a.)

- from AED 0 – AED 50 k

- from AED 51 k – AED 100 k

- from AED 101 k – AED 200 k

- above AED 200 k

--------------

--------------

--------------

--------------

Interest/profit on a car loan (p.a.)

- from AED 0 – AED 50 k

- from AED 51 k – AED 100 k

- from AED 101 k – AED 200 k

- above AED 200 k

--------------

--------------

--------------

--------------

Interest/profit on overdrafts (p.a.)

- from AED 0 – AED 30 k

- from AED 31 k – AED 50 k

- from AED 51 k – AED 100 k

- above AED 100 k

--------------

--------------

--------------

--------------

Interest/profit on unpaid balance on credit card (p.m.)

- from AED 0 – AED 30 k

- from AED 31 k – AED 50 k

- from AED 51 k – AED 100 k

- above AED 100 k

--------------

--------------

--------------

--------------

Appendix No. (2)

Introduction:

- This Amendment applies to and forms part of the Regulations Regarding Bank Loans & Services Offered to Individual Customers (29/2011) (the “Regulations”). It applies specifically to Appendix 2 of those Regulations, which set out the “Maximum Limits for Fees and Commissions Charged on Retail Customer Service”. Upon coming into force, this Amendment replaces the previous version of Appendix 2 and is mandatory and enforceable in the same manner as the Regulations. This Amendment also replaces any other fee caps set out by the Central Bank at this time but not future caps set outside of the scope of this document.

- All fees set out in this Amendment are exclusive of UAE VAT charges.

- Article 11 of 29/2011 remains in force and banks and finance companies must comply accordingly.

- Banks and finance companies will need to notify and seek approval from the CBUAE ex-ante for any planned introduction of a new fee or a change in existing fee levels (which are larger than 5%) not capped by this amendment. Such notifications can be submitted to the CBUAE during the first 5 business days of April and October of any given year.

- The Central Bank will accept ad hoc notifications for exempt fees on an ad hoc basis where it is shown to the Central Bank’s satisfaction that these relate to new products. This will be assessed on a case-by-case basis.

- The fee caps set out in this Amendment represent the maximum permissible charges. Banks and finance companies must have appropriate product approval processes in place for all products, which include an examination of the basis and appropriateness of a fee calculation and, if applicable, must charge lower fees than those prescribed in these caps.

- The Central Bank will supervise regulated entities to ensure that rates are applied in a fair and appropriate manner. This will include ensuring that regulated entities do not automatically default to using maximum caps where actual costs may be lower.

- Regulated entities to which the Regulations apply are required to provide the Central Bank with a full list of the fees they charge no later than 30 days after this Amendment comes into force. Up to date fees should also be made publicly available and should be easily accessible for consumers (e.g. online and in branches).

- These fee caps will be reviewed on an annual basis for continued suitability.

Maximum Limits for Fees and Commissions Charged on Retail Customer Service

No. Product Fee Cap (AED) 1 Personal Accounts Account closure fee 100 2 Personal Accounts Account balance letter 50 3 Personal Accounts No liability certificate 60 4 Personal Accounts Release letter 50 5 Personal Accounts Liability letter issued to Govt Departments/embassies 60 6 Personal Accounts Liability letter issued to financial institutions 60 7 Debit Card Issuing supplementary ATM Card 25 8 Debit Card Replacing Secret Pin Code 25 9 Debit Card Replacing lost or stolen ATM card 25 10 Debit Card Own ATM fees 0 11 Debit Card Fees for using other bank’s ATM 2 12 Debit Card Copy of sales slip 25 13 Consumer Loans Delayed payment penal interest charges Max 200 14 Consumer Loans Early settlement from other bank loans 1% Max 10,000 15 Consumer Loans Final settlement from other sources/EOSB 1% Max 10,000 16 Consumer Loans Partial payment 1% Max 10,000 17 Consumer Loans Revolving overdraft fees 200 18 Consumer Loans Loan Cancellation Fee 100 19 Consumer Loans Other (loan copy, issuing redemption statements, audit confirmation etc) 25 20 Car Loans Early settlement 1% outstanding 21 Car Loans NOC to Traffic Department 0 22 Car Loans Advance payment of installment 1% of installment 23 Car Loans Late payment penal charges Max 500 24 Car Loans Issuance of liability letter to other banks 60 25 Car Loans Cancellation fee 100 26 Remittance Swift copy charges 15 27 Remittance Demand draft/pay order issuance/cancellation 75 28 Customer Term Deposits Account closure fees-terms deposits Cost (max 2%) 29 Credit Cards Card replacement fee 75 30 Credit Cards Liability/no liability letter 50 31 Credit Cards Duplicate statement 45 32 Credit Cards Copy of sales voucher 65 33 Credit Cards Late Payment fees Max 230 34 Home Loans Late payment fees Max 700 35 Home Loans Early settlement fees Max 1% of outstanding balance or 10,000, whichever is less 36 Home Loans Issuance of liability letter 85 37 Home Loans Other certificate 75 38 Home Loans Non-standard statement production/copy of original documentation 100 Home Loans Property swaps administration fee Max 1320

(valuation included)40 Home Loans Issuance of NOC 150 41 Home Loans Partial settlement charges Max 1% of outstanding balance or 10,000, whichever is less 42 Home Loans Clearance letter 95 43 Home Loans Request of other letters 90 - This Amendment applies to and forms part of the Regulations Regarding Bank Loans & Services Offered to Individual Customers (29/2011) (the “Regulations”). It applies specifically to Appendix 2 of those Regulations, which set out the “Maximum Limits for Fees and Commissions Charged on Retail Customer Service”. Upon coming into force, this Amendment replaces the previous version of Appendix 2 and is mandatory and enforceable in the same manner as the Regulations. This Amendment also replaces any other fee caps set out by the Central Bank at this time but not future caps set outside of the scope of this document.

Appendix (3)

Foreign Exchange

Related fees/commissions

Fees for purchase/Sale of currency notes & TC’s (Over & above posted Exchange rates).

Fees on sale of TCs:

- ----------------------.

- ----------------------.

- ----------------------

Fees on issuing Demand Drafts:

Fees on Telegraphic Transfers to:

- India

- Pakistan

- Egypt

- --------

- --------

- -------- etc.